Intro

Choosing the right health insurance plan can be a daunting task, especially with the numerous options available in the market. Two popular types of health insurance plans are HMO (Health Maintenance Organization) and PPO (Preferred Provider Organization). While both plans have their own set of benefits and drawbacks, understanding the key differences between them can help you make an informed decision.

Health insurance is an essential aspect of our lives, providing financial protection against medical expenses. With the rising costs of healthcare, having a suitable health insurance plan can help you avoid financial ruin in the event of unexpected medical emergencies. In this article, we will delve into the world of HMO and PPO plans, exploring their differences, benefits, and limitations.

What is an HMO Plan?

An HMO plan is a type of health insurance that requires you to receive medical care from a network of healthcare providers who have a contract with the HMO. In exchange for lower premiums, you agree to receive care from these in-network providers, who are often paid a fixed fee by the HMO for each patient. HMO plans typically have a primary care physician (PCP) who coordinates your care and provides referrals to specialists within the network.

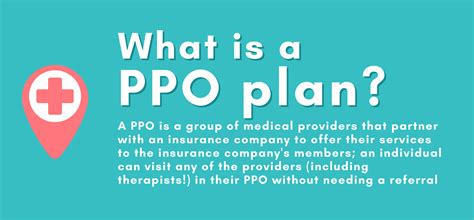

What is a PPO Plan?

A PPO plan, on the other hand, offers more flexibility in choosing healthcare providers. With a PPO plan, you can visit any healthcare provider, both in-network and out-of-network, without a referral from a primary care physician. While PPO plans often have a network of preferred providers, you are not limited to receiving care from these providers. However, you may pay more for out-of-network care.

Key Differences between HMO and PPO Plans

Network and Provider Choice

- HMO plans have a limited network of providers, and you must receive care from these in-network providers to be covered.

- PPO plans have a larger network of providers, and you can visit any healthcare provider, both in-network and out-of-network.

Referrals and Primary Care Physicians

- HMO plans require a primary care physician to coordinate your care and provide referrals to specialists within the network.

- PPO plans do not require a primary care physician, and you can visit any specialist without a referral.

Cost and Premiums

- HMO plans typically have lower premiums due to the limited network and fixed fee payments to providers.

- PPO plans often have higher premiums due to the larger network and flexibility in choosing providers.

Out-of-Pocket Costs

- HMO plans often have lower out-of-pocket costs, such as copays and coinsurance, for in-network care.

- PPO plans may have higher out-of-pocket costs, especially for out-of-network care.

Benefits of HMO Plans

Lower Premiums

- HMO plans often have lower premiums due to the limited network and fixed fee payments to providers.

Coordinated Care

- HMO plans have a primary care physician who coordinates your care and provides referrals to specialists within the network.

Preventive Care

- HMO plans often cover preventive care services, such as annual physicals and screenings, at no additional cost.

Benefits of PPO Plans

Flexibility and Choice

- PPO plans offer more flexibility in choosing healthcare providers, both in-network and out-of-network.

No Referrals Needed

- PPO plans do not require a primary care physician or referrals to visit specialists.

Emergency Care

- PPO plans often cover emergency care, regardless of the provider's network status.

Limitations of HMO Plans

Limited Network

- HMO plans have a limited network of providers, which may limit your choice of healthcare providers.

Referral Requirements

- HMO plans require a primary care physician to coordinate your care and provide referrals to specialists within the network.

Out-of-Network Care

- HMO plans may not cover out-of-network care, or may cover it at a lower rate.

Limitations of PPO Plans

Higher Premiums

- PPO plans often have higher premiums due to the larger network and flexibility in choosing providers.

Higher Out-of-Pocket Costs

- PPO plans may have higher out-of-pocket costs, especially for out-of-network care.

Complexity

- PPO plans can be more complex, with multiple networks and varying levels of coverage.

FAQs

What is the main difference between HMO and PPO plans?

+The main difference between HMO and PPO plans is the network of healthcare providers. HMO plans have a limited network of providers, while PPO plans have a larger network and offer more flexibility in choosing providers.

Do HMO plans cover out-of-network care?

+HMO plans may not cover out-of-network care, or may cover it at a lower rate. It's best to check with your insurance provider to confirm their out-of-network coverage.

Can I visit any specialist with a PPO plan?

+Yes, with a PPO plan, you can visit any specialist without a referral from a primary care physician. However, you may pay more for out-of-network care.

In conclusion, choosing between an HMO and PPO plan depends on your individual needs and preferences. If you prioritize lower premiums and coordinated care, an HMO plan may be the best choice. However, if you value flexibility and choice in healthcare providers, a PPO plan may be the better option. We hope this article has provided you with a comprehensive understanding of the differences between HMO and PPO plans, helping you make an informed decision for your health insurance needs.